Public markets remain an essential component of any diversified portfolio. However, an increasing share of value creation now occurs outside of listed exchanges. Companies are staying private for longer, capital is being deployed more selectively, and many of the most attractive growth opportunities are no longer accessible through traditional public instruments.

At Coventry Management, we provide structured access to alternative investments with a focus on precision, transparency, and alignment. Our approach is not based on broad allocation to opaque vehicles, but on carefully selected opportunities where the underlying assets, structure, and risk profile are clearly understood.

The objective is not simply to participate in private markets, but to do so with a level of control and clarity that is often absent in conventional approaches.

The evolution of global capital markets has materially shifted where and how value is created.

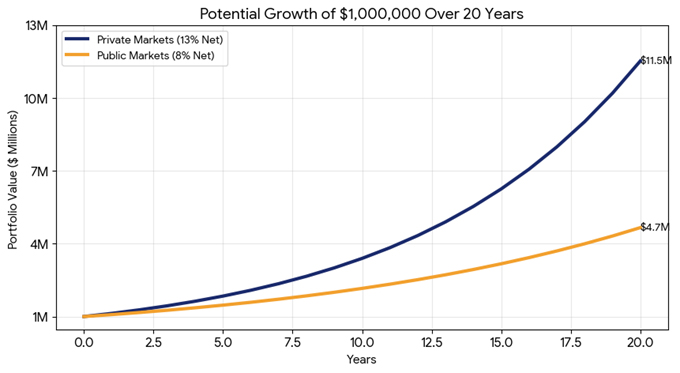

A significant proportion of high-growth companies now raise capital privately, often reaching substantial scale before considering a public listing. By the time an IPO occurs, a large portion of the value creation cycle has already taken place. The "wealth gap" created by private market outperformance (13% avg. net return) vs. traditional public markets (8% avg. return) can be profound over a 20-year horizon (source: Institutional Investor):

At the same time, private equity sponsors, venture capital firms, and institutional investors are increasingly competing for access to these opportunities. This has elevated the importance of sourcing, selectivity, and execution. For investors, this creates both opportunity and risk. Access alone is not sufficient. The quality of the underlying investment and the structure through which it is accessed are equally critical.

Traditional private market investing is typically conducted through blind-pool funds, where capital is committed without visibility into the underlying investments at the time of subscription.

We take a different approach.

Rather than committing capital to a predefined pool, we focus on deal-by-deal participation, allowing clients to evaluate each opportunity on its own merits. This ensures that capital is deployed selectively, with a clear understanding of the business, the sponsor, and the investment thesis.

This approach provides a higher degree of control and avoids the dilution of quality that can occur within broadly diversified funds.

A core component of our offering is direct co-investment alongside established private equity sponsors.

This structure allows clients to invest in specific companies rather than in a fund vehicle. Each opportunity is presented with full transparency, including the underlying business model, financial projections, capital structure, and exit strategy.

A primary driver of co-investment is the superior economic structure.

Traditional private equity funds typically operate on a “2 and 20” model, consisting of a 2% annual management fee and 20% carried interest on profits. These layers of fees can materially reduce net investor returns over time.

Co-investments, by contrast, often bypass these traditional fee structures. In many cases, management fees are reduced or eliminated entirely, and carried interest is either significantly lower or not applied.

The impact on outcomes is meaningful. By reducing fee drag, co-investments can increase net investor gains by up to 26% relative to comparable blind-pool fund exposure.

This structural efficiency is one of the most compelling aspects of direct participation.

Access to high-quality opportunities is not evenly distributed. The most attractive transactions are typically allocated within established networks of sponsors, advisors, and institutional capital providers. Our sourcing capability is built on long-standing relationships within this ecosystem.

This includes:

These relationships allow us to access opportunities that are not broadly marketed. More importantly, they allow us to be selective. The emphasis is on quality over quantity.

Alternative investments require a higher standard of analysis. Information is less standardized, liquidity is limited, and outcomes are more sensitive to execution.

For this reason, our due diligence process is deliberately independent.

A key risk in co-investment is adverse selection, where less attractive deals are offered to external investors while sponsors retain their highest conviction opportunities internally.

To mitigate this, we conduct independent assessment, separate from the lead sponsor’s analysis.

This includes:

We do not rely solely on sponsor-provided materials. Each opportunity must stand on its own merits under independent scrutiny. Only those investments that meet our internal criteria are presented to clients.

In addition to private equity co-investments, we provide access to late-stage private companies and pre-IPO opportunities. These investments offer exposure to businesses that have already demonstrated commercial viability, often with established revenues, institutional backing, and defined paths to liquidity.

Our access is derived from a combination of primary allocations and secondary market transactions. This allows clients to participate in companies that are approaching a potential listing or other liquidity event.

Where appropriate, we also facilitate participation in initial public offerings through institutional channels, providing access that is typically limited to large asset managers.

Different clients have different requirements in terms of ticket size, diversification, and administrative simplicity. While we prioritise direct participation for its transparency and control, we also recognise the importance of flexibility.

Direct stakes provide maximum visibility and control. Clients invest into a specific opportunity, with full clarity on the underlying asset and structure. This approach is particularly suited to those seeking concentrated, high-conviction exposure.

For clients who prefer lower minimums or wish to pool capital into a specific theme, we offer feeder fund structures. These vehicles allow multiple investors to participate in a single opportunity or strategy, while maintaining access to the same underlying assets.

Feeder structures can be particularly effective where:

This flexibility ensures that access to private markets can be tailored without compromising on quality.

Alternative investments carry distinct risks that must be understood and managed.

These include:

Our role is to ensure that these risks are clearly articulated and appropriately incorporated into overall portfolio construction. They are a complement to a broader strategy, designed to enhance long-term returns where appropriate.

Alternative investing is not about accessing more opportunities. It is about accessing the right ones, under the right conditions.

By focusing on direct participation, disciplined due diligence, and efficient structures, we provide a framework that aligns with the expectations of sophisticated investors.

The objective is consistent with all areas of our work. To deploy capital with precision, manage risk with discipline, and ensure that each investment serves a clear purpose within the broader portfolio.

"Before working with Coventry Management, my exposure to private markets was limited to traditional funds, where I had little visibility into what I actually owned.

What changed was the level of transparency and selectivity. Each opportunity is presented with a clear rationale, and I can decide where to participate rather than committing blindly.

The fee structure has also made a meaningful difference. Over time, the reduction in costs has had a noticeable impact on overall returns.

Perhaps most importantly, I feel that the process is controlled. There is a clear framework behind each investment, and that provides a level of confidence that I did not have previously."

Julien M., Luxembourg